Market Cap

$1.10–$1.15B

TTM Revenue Growth

55.36%

PEG Ratio

0.31 fwd / 0.82 trail

Operating Cash Flow

+$40.30M TTM

Forward P/E

11.28–16.92×

EV/EBITDA

17.94–18.80×

Net Cash

$130.30M

Next Earnings

~Aug 2026

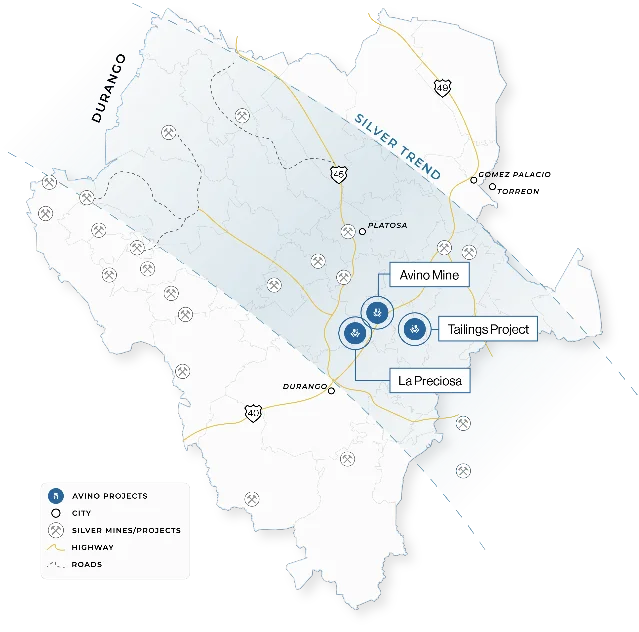

Avino Silver & Gold Mines (NYSE American: ASM) clears all four hard filters with dual-source confirmation — market cap $1.10–$1.15B, TTM revenue +55.36%, forward PEG 0.31 / trailing PEG 0.82, and OCF +$40.30M TTM. The article covers the three-asset Durango, Mexico portfolio (Avino Mine producing, La Preciosa ramping to 500 tpd in H2 2026, Oxide Tailings at pre-feasibility), a $130M net cash fortress balance sheet with Altman Z-Score of 11.99–14.71, eight consecutive quarters of YoY revenue growth, peer valuation context vs. HL/PAAS/CDE, five growth catalysts including the La Preciosa ramp and the June 2026 SVP Corporate Development hire (ex-MAG Silver), five key risks led by silver price sensitivity (5-year beta 2.89) and ongoing ATM dilution, and a Q2 2026 production report (late July) as the primary near-term catalyst.

| Filter | Threshold | Actual | Sources | Verdict |

|---|---|---|---|---|

| Market cap | < $10B | $1.10–$1.15B | StockAnalysis, Yahoo Finance, Finviz | ✅ Pass |

| TTM revenue growth | > 30% | 55.36% | StockAnalysis (55.36%), Finviz (58.64%) | ✅ Pass |

| PEG ratio | < 1.0 | 0.31 (forward) / 0.82 (trailing) | Finviz (only source providing PEG; StockAnalysis / Yahoo show n/a per mining convention) | ✅ Pass |

| Operating cash flow | Positive | +$40.30M TTM | StockAnalysis, Yahoo Finance | ✅ Pass |

| Quarter | Revenue | YoY growth |

|---|---|---|

| Q2'24 | $14.79M | +60.4% |

| Q3'24 | $14.62M | +18.7% |

| Q4'24 | $24.38M | +94.6% |

| Q1'25 | $18.84M | +52.0% |

| Q2'25 | $21.81M | +47.5% |

| Q3'25 | $21.04M | +44.0% |

| Q4'25 | $30.54M | +25.3% |

| Q1'26 | $39.43M | +109.4% |

| Quarter | Net income | EPS (diluted) | Gross margin |

|---|---|---|---|

| Q2'24 | $1.24M | $0.01 | 31.8% |

| Q3'24 | $1.17M | $0.01 | 39.1% |

| Q4'24 | $5.09M | $0.03 | 42.9% |

| Q1'25 | $5.62M | $0.04 | 56.1% |

| Q2'25 | $2.86M | $0.02 | 46.9% |

| Q3'25 | $7.70M | $0.05 | 47.1% |

| Q4'25 | $10.46M | $0.06 | 58.4% |

| Q1'26 | $15.91M | $0.09 | 59.4% |

| Company | Trailing P/E | Forward P/E | EV/EBITDA | P/S | Net margin |

|---|---|---|---|---|---|

| ASM (Avino) | 29.73× | 16.92× | 18.80× | 9.52× | 32.7% |

| HL (Hecla Mining) | 23.13× | 20.33× | 12.05× | 6.52× | 16.8% |

| PAAS (Pan American Silver) | 15.46× | 11.06× | 9.02× | 4.86× | 31.7% |

| CDE (Coeur Mining) | 14.12× | 8.95× | 13.70× | 4.50× | 31.2% |

| Metric | Value | Source |

|---|---|---|

| Cash & equivalents | $138.65M | StockAnalysis 17 |

| Total financial debt | $8.34M (inc. $7.58M leases) | StockAnalysis 17 |

| Net cash | $130.30M ($0.77–0.80/share) | Calculated 17 |

| Total assets | $318.84M | StockAnalysis 17 |

| Shareholders' equity | $275.39M | StockAnalysis 17 |

| D/E ratio | 0.03× | StockAnalysis 1 |

| Current ratio | 5.78× | StockAnalysis 1 |

| Quick ratio | 5.21× | StockAnalysis 1 |

| Interest coverage | 133–148× | StockAnalysis, ROIC.ai 1 |

| Altman Z-Score | 11.99–14.71 | StockAnalysis (11.99), ROIC.ai (14.71) 1 |

| OCF (TTM) | $40.30M | StockAnalysis 12 |

| FCF (TTM) | $12.72M | Calculated (OCF $40.30M – CapEx $27.57M) 12 |

| ROE / ROA / ROIC | 18.12% / 12.48% / 23.04% | StockAnalysis 1 |

| Metric | Value | Source |

|---|---|---|

| Price (Jun 18, 2026 close) | $6.54 | Finviz 3 |

| 52-week high | $11.99 | Finviz 3 |

| Distance from 52-week high | –45.5% | Calculated |

| 52-week low | $3.10 | Finviz 3 |

| YTD performance | +5.3% | Finviz 3 |

| 1-year performance | +85.3% | Finviz 3 |

| 3-year performance | +860.4% | Finviz 3 |

| 50-day moving average | $6.84 (price below) | Finviz 3 |

| 200-day moving average | $6.50 (price above) | Finviz 3 |

| RSI (14-day) | 48.55 | Finviz 3 |

| Beta (5-year) | 2.89 | Yahoo Finance, StockAnalysis 2 |

| Average daily volume | 4.04M–4.94M shares | Multiple sources 3 |

| Short float | 2.81–3.03% | Yahoo Finance, Finviz 2 |

| Days to cover | 0.97–1.08 | Yahoo Finance, Finviz 2 |

| Firm | Action | Price target |

|---|---|---|

| Roth Capital | Target raised $7.50 → $8.00 (May 14, 2026) | $8.00 |

| — | Additional coverage (2 more analysts) | Avg. $11.31 |

| Event | Expected timing |

|---|---|

| Q2 2026 production results | Late July 2026 — first data on La Preciosa 500 tpd ramp progress |

| Q2 2026 earnings | ~August 12, 2026 (Zacks consensus EPS $0.09; 2 analysts revenue est. $57.76M) |

| La Preciosa H2 2026 500 tpd target | H2 2026 (company guidance) |

| Possible resource update | H2 2026 (post-30,000m drill program) |

| H.C. Wainwright Global Investment Conference | September 14–16, 2026 |

| Beaver Creek Precious Metals Summit | September 22–25 (David Wolfin presenting September 23) |

| New Orleans Investment Conference | October 28–31, 2026 |

| NCIB buyback window | April 8, 2026 – April 7, 2027 |

Add more perspectives or context around this Post.